Ericsson Phone 1931

Product Offerings, Life Cycle and Supply Chain

Products do not last forever. Consider the telephone, for example. While the 1931 Ericsson phone (pictured) is no longer in existence, it has given way to far more sophisticated desktop phones, mobile phones and smartphones. Over the past 100+ years, the phone as a medium of communication has evolved considerably – with the introduction of many models, features and technological innovations – since the groundbreaking era of Alexander Graham Bell.

When a product is first introduced, it typically has a high cost due to the initially-low production run, and the high costs associated with product development. The search for early-adopters of a new product have a considerable impact on the marketing strategy. As the product grows and matures, the marketing strategy changes, as it does again when the product is in decline. At each stage throughout the product life cycle, the marketing of the product changes to meet the challenges of that stage.

Value Proposition & Supply Chain

When a new product is developed, a company must research and develop the “value proposition” to its customers and communicate its value. A value proposition is a promise of value to be delivered and acknowledged. It is also a belief from the customer how value (benefit) will be delivered and experienced. A value proposition can apply to an entire organization, or parts thereof, or customer accounts, or products or services.

In addition to considering the competitive landscape, and where their product fits in, marketers must always ask where a new product will fit into their current lineup of product / service offerings, and how it can support or complement the existing brand.

BMW, for example, makes a range of sporty luxury vehicles aimed at the upper-middle and wealthy classes. Developing an inexpensive and lower-quality vehicle to compete with cars in another class may dilute the BMW brand and hurt sales. However, if BMW were to market the vehicle under a different brand, they could diversify their product portfolio, avoid the risk of diluting the BMW brand, and be able to reach new customers all at the same time. Some firms go to great lengths to disassociate their brands from one another, while others embrace a family of brands model. These decisions vary by industry and business and marketing strategy.

Equally important in delivering value to the customer through an offering is how a company sources the goods and services necessary for production and delivers the end product for customers to purchase – otherwise known as the supply chain. A supply chain is a system of organizations, people, activities, information, and resources involved in moving a product or service from supplier to customer. Supply chain activities involve the transformation of natural resources, raw materials, and components into a finished product that is delivered to the end customer.

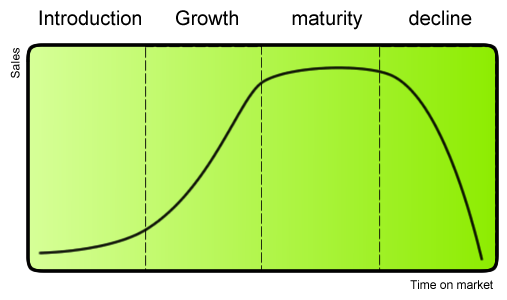

Product Life Cycle

The concept of product life cycle (PLC) concerns the life of a product in the market with respect to business/commercial costs and sales measures. The product life cycle proceeds through multiple phases, involves many professional disciplines, and requires many skills, tools and processes. PLC management makes the following three assumptions:

- Products have a limited life and thus every product has a life cycle.

- Product sales pass through distinct stages, each posing different challenges, opportunities, and problems to the seller.

- Products require different marketing, financing, manufacturing, purchasing, and human resource strategies in each life cycle stage.

Characteristics of PLC stages

The four main stages of a product’s life cycle and the accompanying characteristics are:

| Stage

|

Characteristics

|

| Market introduction stage

|

- costs are very high

- slow sales volumes to start

- little or no competition

- demand has to be created

- customers have to be prompted to try the product

- makes little money at this stage

|

| Growth stage

|

- costs reduced due to economies of scale

- sales volume increases significantly

- profitability begins to rise

- public awareness increases

- competition begins to increase with a few new players in establishing market

- increased competition leads to price decreases

|

| Maturity stage

|

- costs are decreased as a result of production volumes increasing and experience curve effects

- sales volume peaks and market saturation is reached

- increase in competitors entering the market

- prices tend to drop due to the proliferation of competing products

- brand differentiation and feature diversification is emphasized to maintain or increase market share

- industrial profits go down

|

| Saturation and decline stage

|

- costs become counter-optimal

- sales volume decline

- prices, profitability diminish

- profit becomes more a challenge of production/distribution efficiency than increased sales

Note: Product termination is usually not the end of the business cycle, only the end of a single entrant within the larger scope of an ongoing business program.

|

The purpose of this learning pathway is to help you understand the importance of developing a value proposition throughout a product’s life cycle and the supply chain necessary to deliver it to the end-user. You will learn to:

- Define a product life cycle and its stages.

- Explain a value proposition and how it changes throughout the product life cycle, whether for business-to-business (B2B) or business-to-consumer (B2C) customers.

- Examine supply chain functions to determine their appropriateness in terms of cost, delivering value and contributing to profitability.

Product Offerings, Life Cycle and Supply Chain

Products do not last forever. Consider the telephone, for example. While the 1931 Ericsson phone (pictured) is no longer in existence, it has given way to far more sophisticated desktop phones, mobile phones and smartphones. Over the past 100+ years, the phone as a medium of communication has evolved considerably – with the introduction of many models, features and technological innovations – since the groundbreaking era of Alexander Graham Bell.

When a product is first introduced, it typically has a high cost due to the initially-low production run, and the high costs associated with product development. The search for early-adopters of a new product have a considerable impact on the marketing strategy. As the product grows and matures, the marketing strategy changes, as it does again when the product is in decline. At each stage throughout the product life cycle, the marketing of the product changes to meet the challenges of that stage.

Value Proposition & Supply Chain

When a new product is developed, a company must research and develop the “value proposition” to its customers and communicate its value. A value proposition is a promise of value to be delivered and acknowledged. It is also a belief from the customer how value (benefit) will be delivered and experienced. A value proposition can apply to an entire organization, or parts thereof, or customer accounts, or products or services.

In addition to considering the competitive landscape, and where their product fits in, marketers must always ask where a new product will fit into their current lineup of product / service offerings, and how it can support or complement the existing brand.

BMW, for example, makes a range of sporty luxury vehicles aimed at the upper-middle and wealthy classes. Developing an inexpensive and lower-quality vehicle to compete with cars in another class may dilute the BMW brand and hurt sales. However, if BMW were to market the vehicle under a different brand, they could diversify their product portfolio, avoid the risk of diluting the BMW brand, and be able to reach new customers all at the same time. Some firms go to great lengths to disassociate their brands from one another, while others embrace a family of brands model. These decisions vary by industry and business and marketing strategy.

Equally important in delivering value to the customer through an offering is how a company sources the goods and services necessary for production and delivers the end product for customers to purchase – otherwise known as the supply chain. A supply chain is a system of organizations, people, activities, information, and resources involved in moving a product or service from supplier to customer. Supply chain activities involve the transformation of natural resources, raw materials, and components into a finished product that is delivered to the end customer.

Product Life Cycle

The concept of product life cycle (PLC) concerns the life of a product in the market with respect to business/commercial costs and sales measures. The product life cycle proceeds through multiple phases, involves many professional disciplines, and requires many skills, tools and processes. PLC management makes the following three assumptions:

Characteristics of PLC stages

The four main stages of a product’s life cycle and the accompanying characteristics are:

Note: Product termination is usually not the end of the business cycle, only the end of a single entrant within the larger scope of an ongoing business program.

Objectives

The purpose of this learning pathway is to help you understand the importance of developing a value proposition throughout a product’s life cycle and the supply chain necessary to deliver it to the end-user. You will learn to:

Content is available under the

Creative Commons Attribution Share Alike License.

Privacy Policy | Authors